🕑 5 min read

Wall Street isn’t waiting for the crypto recovery. It’s building something else entirely.

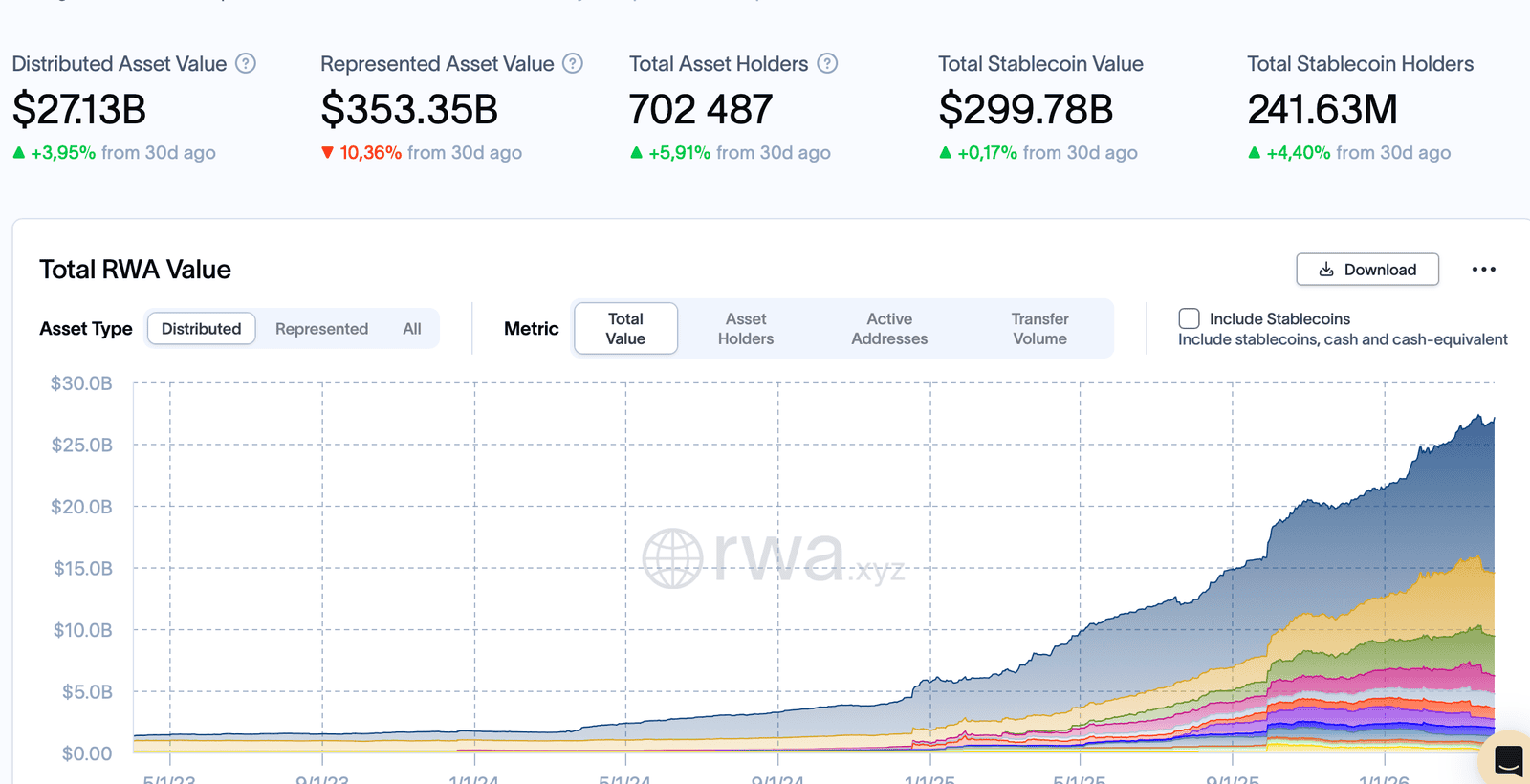

Forget the price charts for a second. While Bitcoin bleeds 47% from its all-time high and Crypto Twitter argues about whether $67,000 is a bottom or a trap, something genuinely unprecedented is happening in the background. Tokenized real-world assets just crossed $27.13 billion in distributed on-chain value as of March 31, 2026 – a fourfold increase from a year ago, with 702,487 asset holders and growing.

That’s not DeFi speculation. That’s not memecoin money. That’s BlackRock, Goldman Sachs, JPMorgan, and Franklin Templeton moving U.S. Treasuries, home loans, corporate bonds, and ETFs onto blockchain rails. And they’re accelerating.

The crypto market lost roughly $1.2 trillion in market cap since January’s highs. The tokenized asset market gained $20 billion over the same period. If you’re only watching BTC/USD, you’re missing the real story.

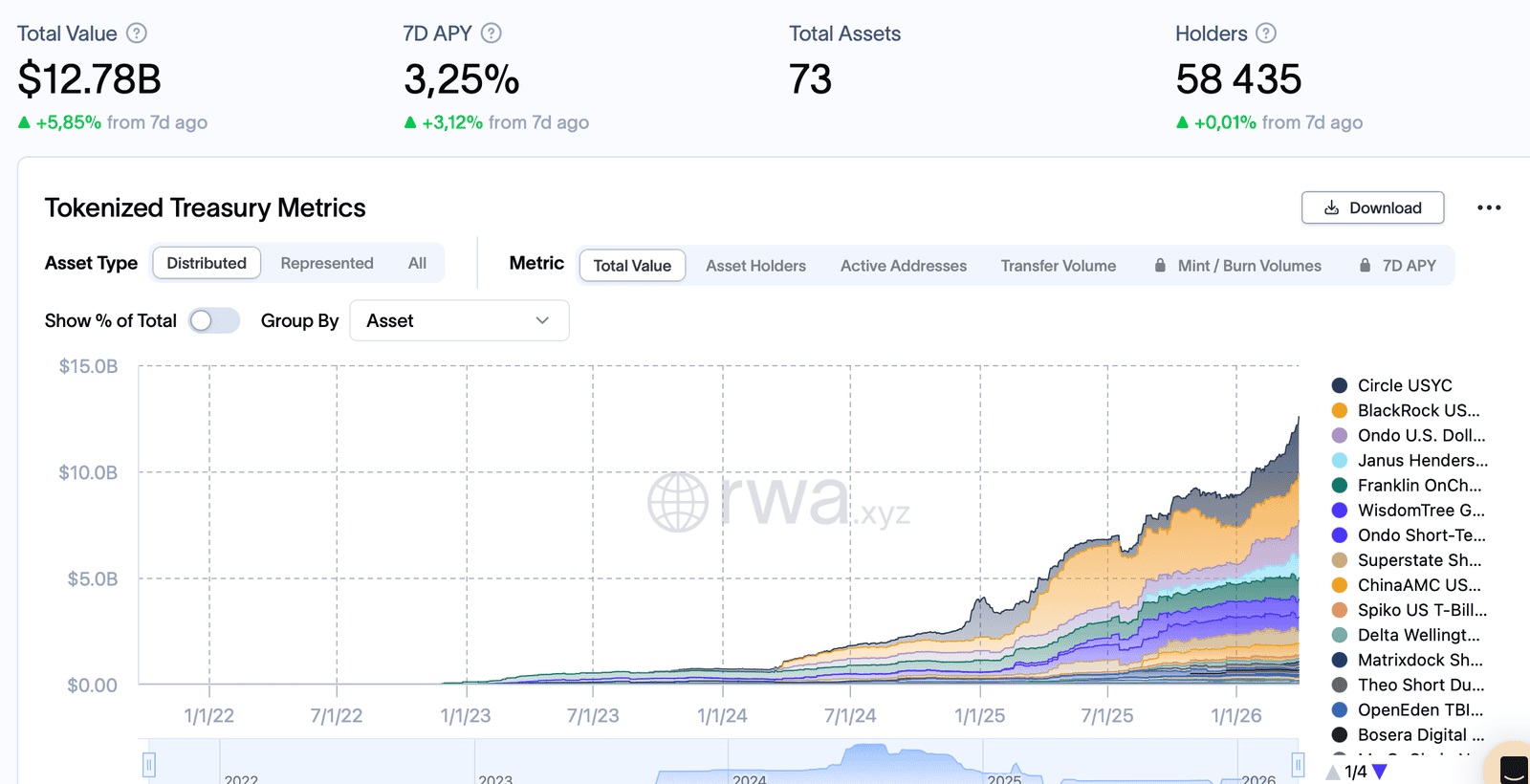

The $12.78 Billion Treasury Migration

Tokenized U.S. Treasuries surged to $12.78 billion – up 6.85% in just the past week – with 73 different products and 58,435 holders earning a 3.25% average yield. That’s government debt, the most boring financial instrument on the planet, living on Ethereum, Solana, and Arbitrum.

BlackRock’s BUIDL fund, a tokenized money market product built with Securitize, now holds over $2 billion across nine blockchain networks. It’s paid out roughly $100 million in dividends since launch. And in February, BUIDL became tradable on Uniswap – yes, the DeFi protocol – allowing whitelisted investors to swap in and out using stablecoins around the clock.

But BlackRock isn’t even winning this race anymore.

Circle’s USYC overtook BUIDL back in January, hitting $1.69 billion before BUIDL clawed its way back. Ondo Finance – which now commands $2.5 billion in total value locked – partnered with Franklin Templeton on March 25 to tokenize five ETFs from a $1.7 trillion asset manager. Those ETFs trade 24/7 in crypto wallets across Europe, Asia-Pacific, and Latin America.

“Tokenized US Treasuries silently replaced DeFi’s foundation,” CryptoSlate reported in their analysis of the shift. And they’re right – what started as a $4.8 billion niche at the start of 2025 quietly ballooned into a $12.78 billion market that most crypto traders still haven’t noticed.

A $16.5 Billion Home Loan on a Blockchain

Want to know how real this trend has gotten? Look at Figure HELOC.

FIGR_HELOC, a token representing fractional ownership in a portfolio of home equity lines of credit, sits at the #9 spot on CoinGecko with a $16.5 billion market cap. That’s bigger than Cardano ($9B). Bigger than Chainlink ($6.2B). Bigger than Monero ($6.1B).

Figure Technologies went public on Nasdaq in September 2025 at $25 a share – it now trades above $31. The company has originated over $16 billion in cumulative home equity loans, all processed on the Provenance blockchain. When a homeowner in Ohio takes out a HELOC through Figure’s platform, that loan gets pooled, tokenized, and sold to investors who collect the interest payments.

“Figure Heloc becomes 10th biggest crypto – but critics say it shouldn’t be there,” Yahoo Finance noted. And the critics have a point – it’s not a cryptocurrency in any traditional sense. It’s a securitized lending product that happens to settle on-chain. But that’s precisely what makes it significant. The lines between “crypto” and “traditional finance” aren’t blurring anymore. They’re gone.

Goldman, JPMorgan, and the Collateral Revolution

The institutional adoption isn’t theoretical anymore – it’s operational.

Goldman Sachs now uses tokenized U.S. Treasuries as collateral in derivatives transactions through the Canton Network, where over 30 institutions piloted tokenized bonds and gold. JPMorgan’s Onyx platform has processed billions in tokenized collateral for wholesale payments and liquidity management.

For context: when Goldman accepts a tokenized Treasury as collateral instead of a physical bond, they’re bypassing the entire settlement infrastructure that’s existed since the 1970s. No custodian delays. No T+2 settlement. No faxes – and yes, Wall Street still uses faxes.

Morgan Stanley is planning to launch a tokenized asset wallet in 2026. Deutsche Bank, HSBC, Citigroup, and Standard Chartered are all running their own tokenization initiatives.

And here’s the regulatory tailwind that ties it together: Congress passed the CLARITY Act regulatory framework in late March, establishing clear rules for tokenized securities. Combined with the GENIUS Act – which already fueled the stablecoin market past $320 billion – the regulatory infrastructure for on-chain finance is falling into place faster than anyone expected.

The $100 Billion Question

McKinsey projects the tokenized asset market could reach $2 trillion by 2030. But the nearer-term number matters more: analysts are targeting $100 billion by end of 2026.

That’s a 4x from current levels in nine months. Aggressive? Sure. But consider the trajectory – the market went from $6.7 billion to $27.1 billion in twelve months with barely any retail participation. This is almost entirely institutional capital.

Ethereum still dominates with $12.8 billion in RWA value locked, followed by BNB Chain at $2 billion. Solana is gaining ground fast thanks to the BUIDL expansion and Ondo’s integration. Provenance, Figure’s chain, quietly holds the largest single-asset tokenized portfolio.

Where does this leave Bitcoin? Possibly in a very different conversation than the one happening on Twitter. BTC’s MVRV ratio sits at 1.23, exchange reserves climbed to 2.71 million BTC, and NUPL hovers at 0.188 – all near cycle lows. The crypto market is pricing in pain.

But the institutional money isn’t leaving blockchain. It’s just moving to a different part of it – one where yields come from Treasury coupons and mortgage payments instead of token emissions and leverage.

The next catalyst lands in July: the GENIUS Act’s regulatory deadline, which could unlock the next wave of bank-issued stablecoins and tokenized products. If the first $27 billion came with regulatory ambiguity, imagine what happens with clarity.

This is not financial advice. DYOR. Data as of March 31, 2026.

Sources:

- RWA.xyz – Real-World Asset Analytics

- RWA.xyz – Tokenized U.S. Treasuries

- CoinGecko – Figure HELOC Market Data

- BlackRock BUIDL Fund – Securitize

- Franklin Templeton x Ondo – Tokenized ETFs

- CryptoSlate – Tokenized Treasuries Replace DeFi Foundation

- Yahoo Finance – Figure HELOC Becomes 10th Biggest Crypto

- CryptoQuant – BTC Market Indicators

Leave a Reply