🕑 6 min read

Scroll through r/CoinBase for five minutes and you’ll spot the same post repeated dozens of times with slight variations: “Why did I just pay $47 in fees on a $1,000 buy?” The top comment is always some version of the same three words — “Switch to Advanced.”

That pretty much captures the Coinbase fee situation in 2026. The exchange is NASDAQ-listed, FDIC-insured, hasn’t been breached in over a decade — and bleeds casual users through a fee structure so layered that most people don’t realize how much they’re losing until they do the math themselves. We dug through every charge Coinbase levies, from the trading fees you can see to the staking commissions you definitely can’t, and the full picture deserves more attention than it gets.

The fee Coinbase doesn’t put on your receipt

Every Simple Trade conversion has a cost that never appears as a line item. Coinbase calls it the “spread” — roughly 0.50% baked into the quoted price. You won’t find it on the preview screen, you won’t see it in your transaction history, and unless you’re comparing the execution price against another exchange in real time, you’d never notice it.

On a $10,000 BTC buy, about $50 vanishes into that spread before the actual trading fee even kicks in.

And no, that’s not a typo.

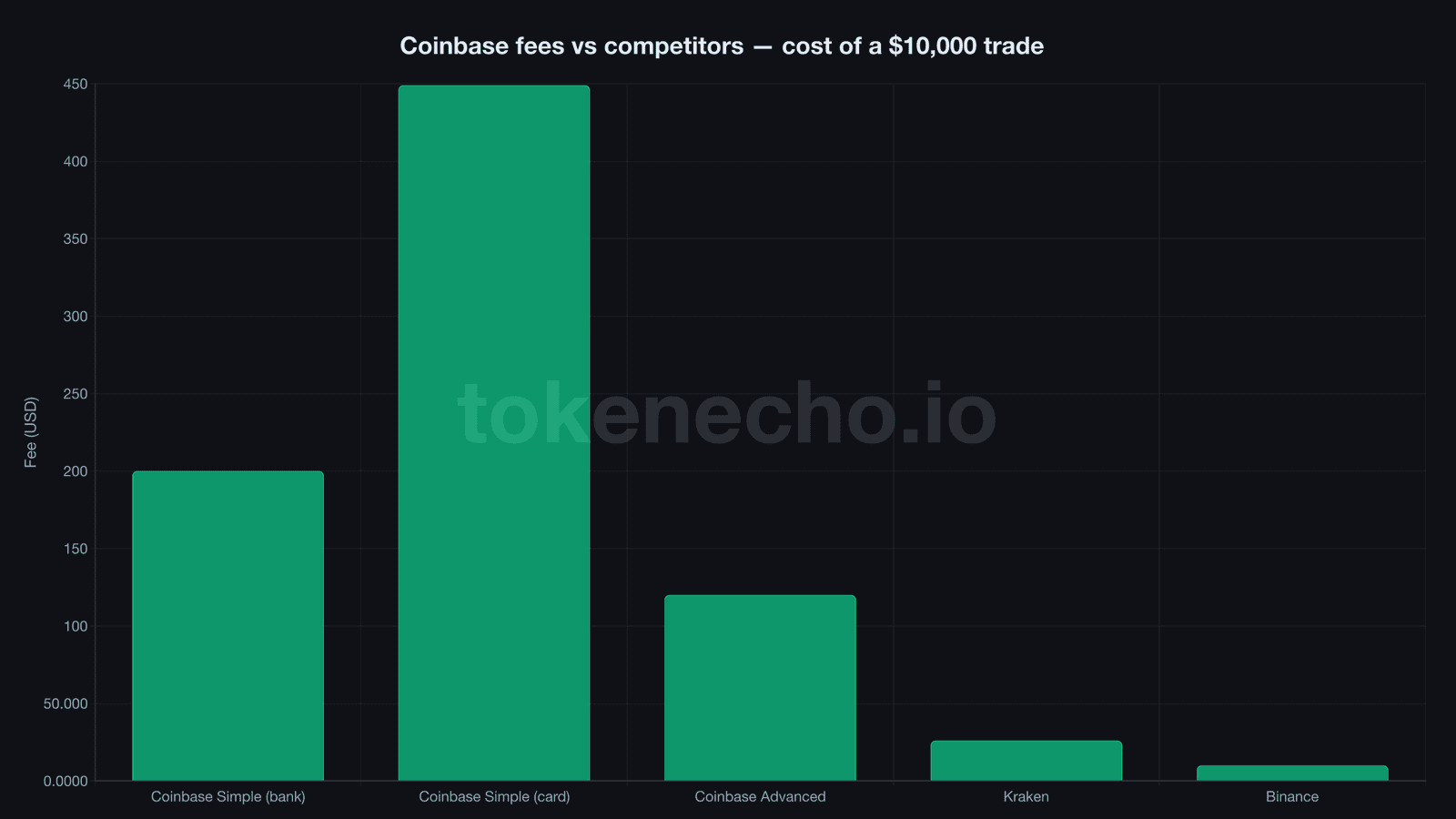

Combine the spread with the percentage-based charge — 1.49% for bank transfers, a punishing 3.99% for debit cards — and Simple Trade’s true cost lands somewhere between 2% and 4.5% per transaction.

The same roundtrip on Binance costs about 0.20%. We checked twice.

Same app, same login — one costs twelve times more

“120 basis points??? Coinbase’s fees are outrageous,” said Alex Svanevik, CEO of blockchain analytics firm Nansen, in a January 2026 post on X — right after discovering his account had been quietly migrated to the base Advanced Trade tier without notification, a change that affected thousands of previously lower-fee traders overnight.

The irony: even Svanevik’s “outrageous” 1.20% taker fee is less than half of what Simple Trade costs on a bank purchase.

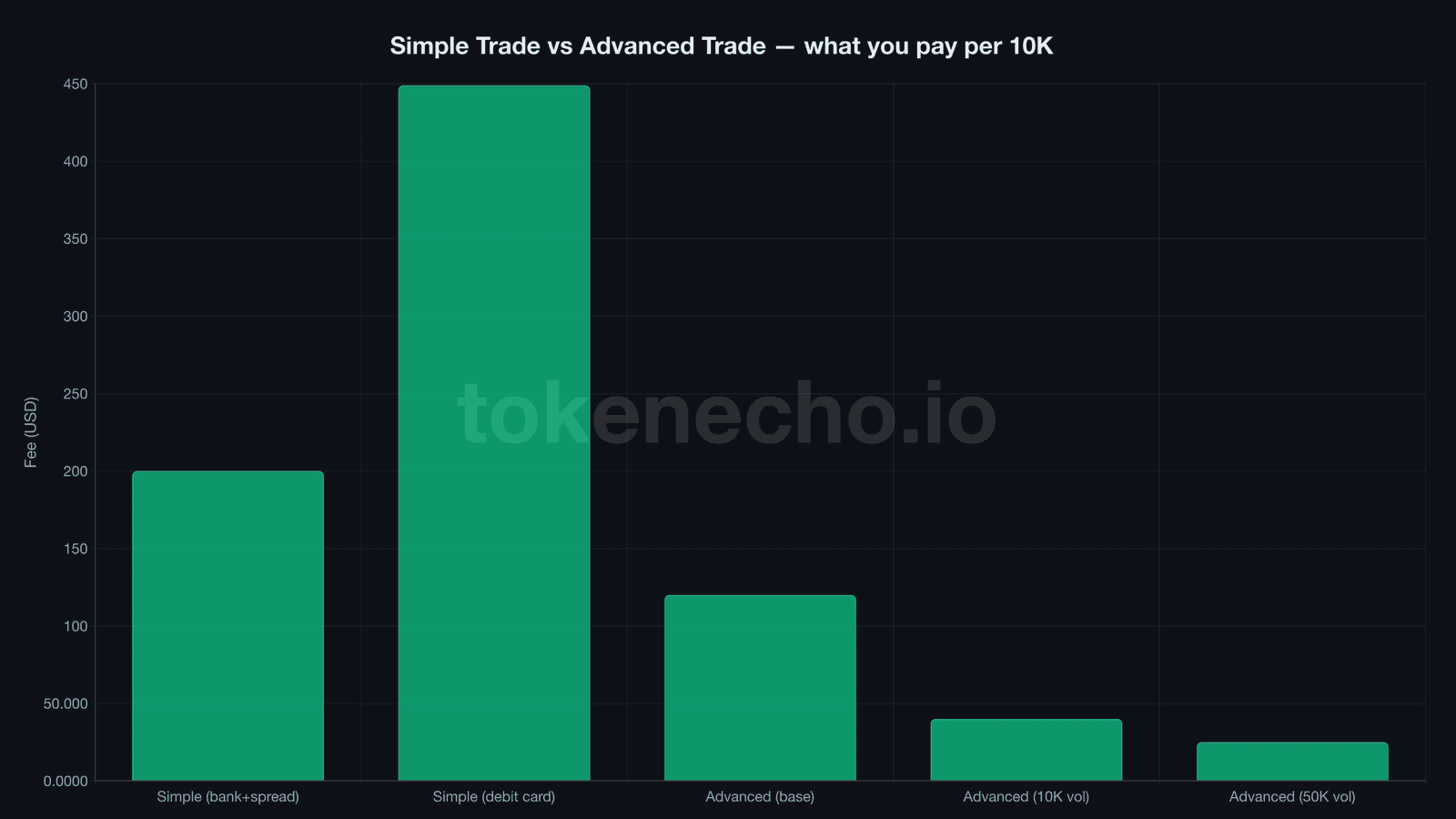

Coinbase runs two entirely separate trading interfaces inside the same application. Same account. Same coins. Simple Trade — the one most users land on by default — charges flat fees on small orders ($0.99 on a $10 buy, effectively a 10% tax) and percentage fees on everything else.

Advanced Trade uses a maker/taker model. Base tier: 0.60% maker, 1.20% taker. Steep — but the spread disappears completely. Switching takes about 30 seconds, and that alone cuts most users’ costs in half.

Push past $10,000 in monthly volume and fees drop to 0.25%/0.40%. At the very top — $250 million monthly, which is firmly institutional territory — you’re trading at 0.05% taker.

Nobody reading this trades $250 million a month.

A trader moving $5,000 monthly pays $20-30 on Coinbase Advanced. The same volume on Kraken costs $8-13. On Binance, about $5. Switching interfaces doesn’t close that gap entirely — but it’s the single biggest fee cut available to any Coinbase user, and it costs nothing.

Your staking yield lost 35% before you ever saw it

$0. That’s what Coinbase charges for staking, according to the app.

No disclosure. No line item. Just a clean APY number sitting next to each asset: 2.2% on ETH, roughly 7% on SOL. Looks reasonable.

Except those numbers are already net of commission. Coinbase takes 25% off ETH rewards before displaying your yield. On SOL, ADA, DOT, ATOM, AVAX? The cut jumps to 35%.

Stake the same SOL through a non-custodial validator like Jito and you’d earn north of 7.4% with zero commission. Coinbase shows you roughly 7%. Over a year on a $5,000 stake, that gap compounds into a couple hundred dollars — real money that quietly redirected itself to Coinbase’s balance sheet.

Want out early? A 1% instant unstaking fee on the total amount. DOT locks you up for 28 days if you’d rather not pay. The whole setup works the same way gym contracts do — designed so leaving costs more than staying, even after you’ve stopped going.

A brief tangent about how Coinbase actually makes money

Coinbase pulled $7.2 billion in revenue during fiscal year 2025. S&P Global broke down the split: $4.2 billion — 59% of every dollar the company earned — came from transaction fees. Back when Coinbase IPO’d in April 2021 at a $85 billion valuation, that number was 96%.

The company has spent five years trying to diversify into subscriptions, staking custody, and USDC interest revenue. It’s working — subscription revenue hit $2.8 billion, up 23% year over year. But the core business still runs on retail users paying Simple Trade rates. When Coinbase restructured its Advanced Trade tiers in January 2026, pushing users into higher fee brackets, the message was clear enough: they need you on the expensive interface. That’s the model.

The 3.99% impulse tax and other ways money leaks out

Why does anyone pay 3.99% just to deposit money into Coinbase?

Because ACH takes 1-3 business days and a debit card clears instantly. Bitcoin’s down 8% at 2 AM on a Sunday and you want in now, not Tuesday. Same markup airports put on bottled water — they know you’re not walking to the gas station across the highway.

ACH transfers are free both ways. Genuinely the only bargain on the platform, and the only funding method worth using.

Wires cost $10 in, $25 out. Instant cashout to a debit card runs up to 1.5%.

The Visa debit card — not the Coinbase One Card, completely different product — charges 2.49% every time you spend crypto that isn’t USDC.

Tack on the 0.20% domestic commission and each swipe costs 2.69%. International? Add another 3%. The 1-4% crypto rewards partially offset this, but “partially” is pulling a lot of weight in that sentence.

Crypto deposits are free. Crypto withdrawals charge only the network fee. At least something doesn’t come with a surcharge.

Coinbase One only pays off past $3,000 a month

Three tiers since January 2026. Basic runs $4.99 monthly and waives Simple Trade fees on the first $500 in purchases.

The savings at that volume? About four bucks. You’re essentially paying Coinbase to break even.

Preferred costs $29.99 a month and extends zero-fee Simple Trade to $10,000 monthly. The staking commission also drops — 28.50% instead of the standard 35%. For anyone trading $3,000 or more per month, the math actually starts working.

600,000 members had joined by early 2026. But for the person buying $200 of BTC every paycheck?

Skip it.

The newest Coinbase One Card — an American Express credit card launched late 2025 — pays 2-4% back in BTC depending on your asset balance. No liquidation fee. But it requires the subscription, and the elevated rewards cap at $10,000 in monthly purchases. You’d need to run serious volume through the card for the BTC-back to meaningfully offset the $49.99 annual cost.

For the complete tier breakdown, see our Coinbase Advanced Trade fees guide. For how Coinbase stacks up against competitors, read our Coinbase vs Kraken vs Binance comparison.

Coinbase charges a premium for being the exchange your parents’ financial advisor has actually heard of. Whether that brand tax justifies paying 12x what Binance charges — that’s between you and your transaction history.

This is not financial advice. DYOR. Data as of April 10, 2026.

Sources:

Leave a Reply