🕑 4 min read

LTH-SOPR hit 0.76 on March 27.

That number might not mean much unless you’ve been watching it daily. Long-term holders – wallets that haven’t moved their Bitcoin in over 155 days – just sold coins at an average loss of 24%. These aren’t panic-selling retail traders who aped in last month. These are the diamond hands. The HODLers. The ones who sat through Luna’s implosion, FTX’s bankruptcy, and COVID’s March 2020 crash without flinching.

They’re flinching now.

From 94% Profit to 24% Loss in Five Days

On March 22, LTH-SOPR, a metric tracking the profit ratio of long-term holder transactions, printed 1.94. That meant every coin these veterans moved was sold at nearly double their cost basis. Five days later? The metric cratered to 0.76 – a swing so violent it resembles someone slamming the brakes on a highway and immediately throwing the car into reverse.

This isn’t the first time this month, either. On March 11, LTH-SOPR briefly touched 0.639 – a 36% average loss. CryptoQuant contributor The Enigma Trader flagged it as “one of the strongest capitulation signals in recent months.” The metric recovered, briefly. Then it broke again.

Two LTH capitulation events in 17 days. That hasn’t happened since late 2022.

The Accumulation Narrative Just Broke

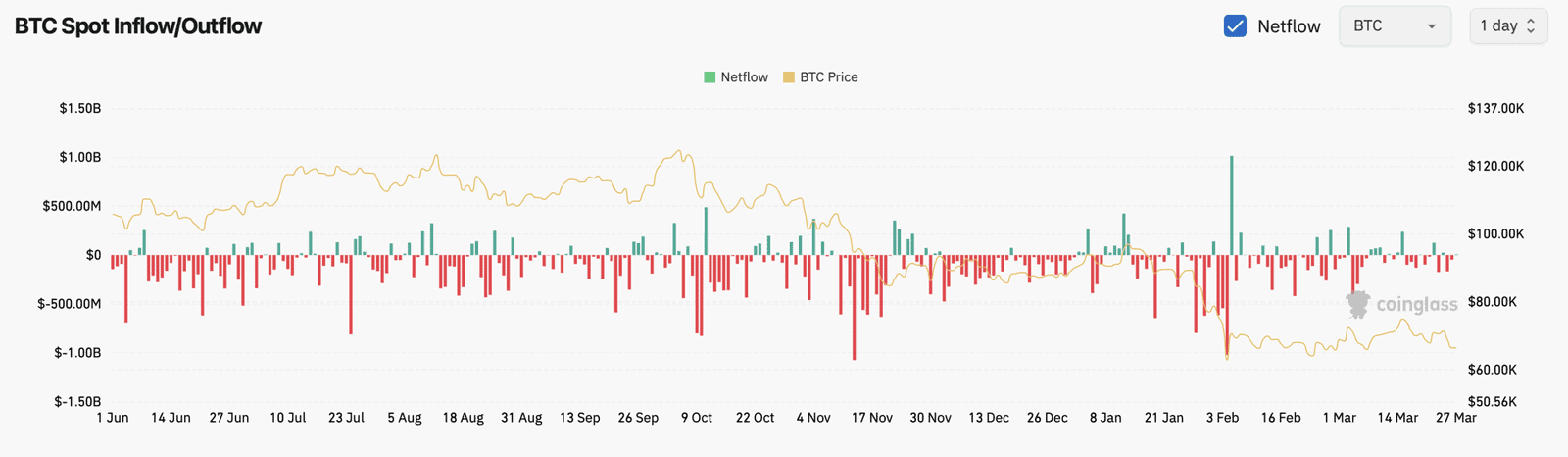

For weeks, the dominant story across crypto media was simple: whales are buying, exchange reserves are dropping, smart money is accumulating. And the data supported it – between March 22 and March 25, a net 23,100 BTC flowed off exchanges. Classic accumulation behavior.

Then it stopped.

March 26: +1,693 BTC flowed back onto exchanges. March 27: +213 BTC. March 28: +999 BTC. Three consecutive days of net inflows – the first such streak since early March. Coins are moving back to trading venues, which historically signals increased sell pressure ahead.

“Bitcoin is not in a position to be pumped,” CryptoQuant CEO Ki Young Ju said earlier this month, projecting “prolonged sideways consolidation rather than an imminent crash.” The exchange flow data now backs that assessment with receipts.

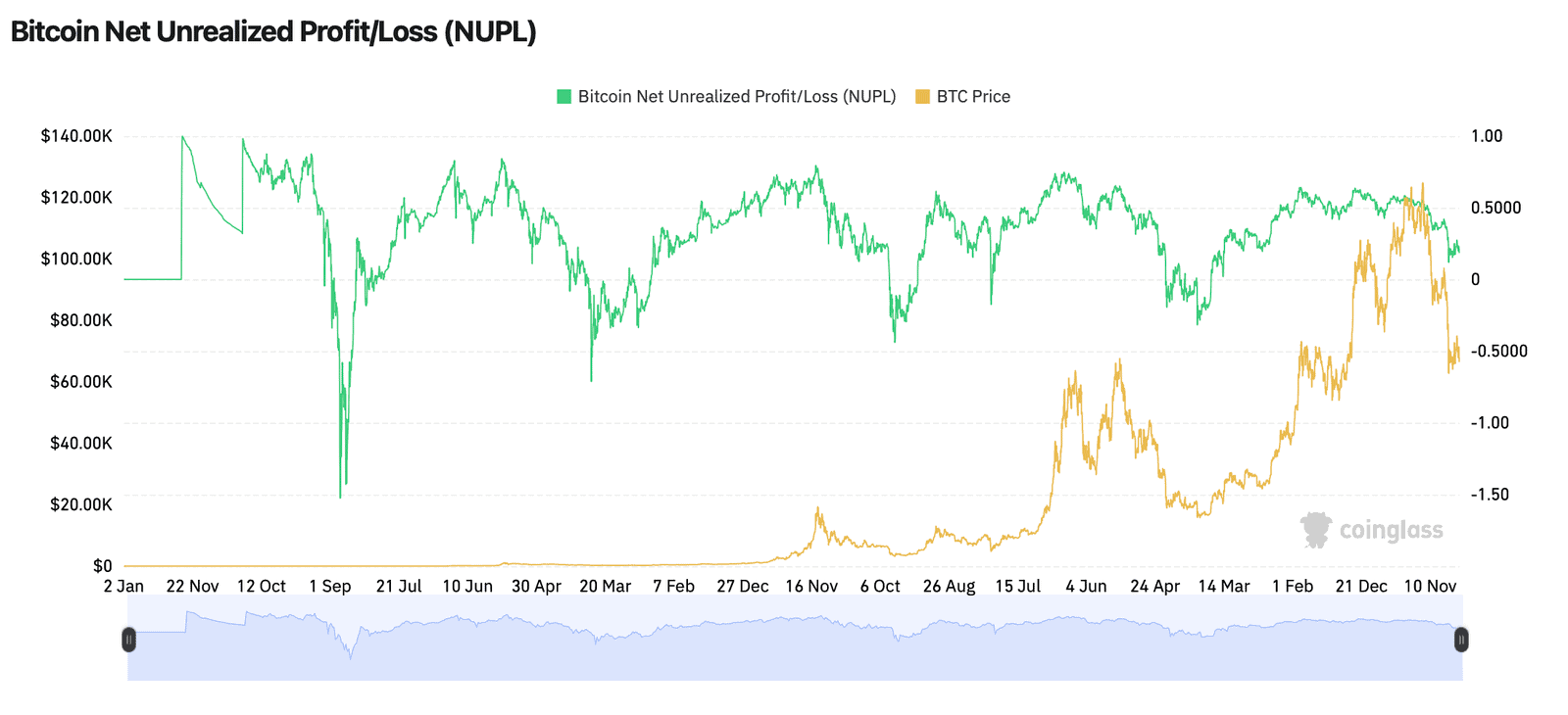

NUPL Is Sliding Toward the Capitulation Zone

Net Unrealized Profit/Loss, a gauge of how much of the network sits in profit versus loss, dropped to 0.183 on March 27. That’s down from 0.238 just three days earlier. For context, NUPL below 0.25 puts the market firmly in “fear” territory. Below zero? That’s full capitulation.

We’re not there yet. But the trajectory is unmistakable.

MVRV, which compares Bitcoin’s market price to its realized price, the average cost basis of every coin on-chain, sits at 1.22 and declining. BTC at $66,417 trades roughly 22% above the network’s aggregate cost basis of $54,233 – still a cushion, but one that’s thinning daily.

On March 8, NUPL briefly hit 0.174. The current reading of 0.183 is dangerously close to retesting that level. If it breaks below, the market enters a zone where more than half of all coins are underwater.

So Why Isn’t This Bearish Enough to Panic?

Because the ammunition for a rebound is stacking up in the background.

The Stablecoin Supply Ratio dropped to 9.74 on March 27 – the lowest level this month. A declining SSR means stablecoin market capitalization is growing relative to Bitcoin’s. Translation: there’s more dry powder sitting on the sidelines than at any point in March. That $184 billion USDT market cap and $77.8 billion USDC aren’t just sitting idle. They’re potential buy orders waiting for a catalyst.

ETF holdings remain stubbornly stable at 1.32 million BTC. Despite retail panic, despite LTH capitulation, despite exchange inflows – institutional allocators haven’t blinked. BlackRock’s IBIT and the new staked ETHB product continue absorbing inflows while competitors bleed.

And the Puell Multiple, measuring daily miner revenue against its 365-day average, reads 0.72. Miners are stressed but not yet in the extreme zone below 0.5 that marked previous cycle bottoms. The pressure is building, not breaking.

The Historical Rhyme Nobody’s Drawing

March 11: LTH-SOPR hits 0.639. March 22: it spikes to 1.94 as some holders take profit on a brief rally. March 27: it crashes again to 0.76. This whipsaw pattern – capitulation, relief, deeper capitulation – is textbook late-stage bear behavior.

The last time Bitcoin saw consecutive LTH capitulation events this close together was November-December 2022, in the immediate aftermath of FTX’s collapse. BTC was trading around $16,500 then. Within three months it was back above $23,000. Within twelve months, it had crossed $40,000.

Does that mean $66,000 is the new $16,500? Not necessarily. The macro backdrop is different – 10-year Treasuries at 4.5%, an active geopolitical crisis with Iran, and a Fed that won’t budge on rates. But the on-chain structure rhymes. LTH capitulation exhausts sell pressure. Rising stablecoin reserves provide the fuel. And exchange flows, once they reverse again from inflows back to outflows, tend to confirm the bottom retroactively.

Willy Woo, one of crypto’s most respected on-chain analysts, projects a bear market floor around $45,000, with potential downside to $30,000 “should macro conditions deteriorate further.” If he’s right, the current LTH capitulation is just the opening act.

If he’s wrong – and the $54,233 realized price holds as support – then long-term holders selling at a 24% loss will look like the same mistake retail made at $16,500 in November 2022.

Bitcoin’s realized price hasn’t been breached since the FTX crash. Whether that $54K floor holds may determine if this capitulation was the end of the pain – or just intermission.

This is not financial advice. DYOR. Data as of March 28, 2026.

Sources

- CryptoQuant API – LTH-SOPR, exchange netflows, NUPL, MVRV, SSR, realized price, Puell Multiple, ETF holdings (accessed March 28, 2026)

- CoinGecko API – BTC price $66,417, market cap $1.33T, 24h volume $36.3B (accessed March 28, 2026)

Leave a Reply