Gold Crashes 14% While AI Tokens Surge 80% – The Data Behind Crypto’s Great Rotation

🕑 6 min read

March 2026 broke the old playbook. Not bent it, not tested it – broke it completely.

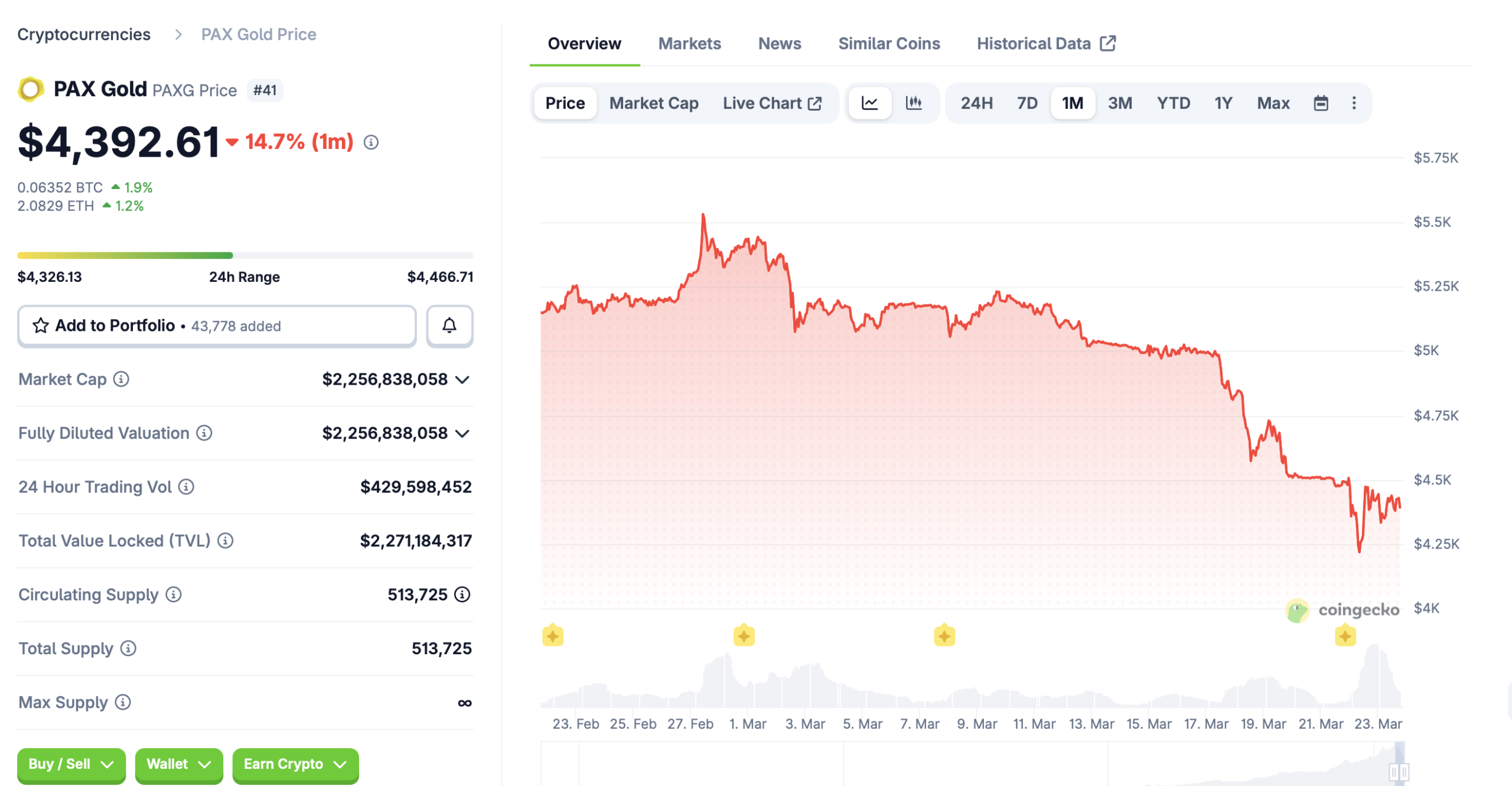

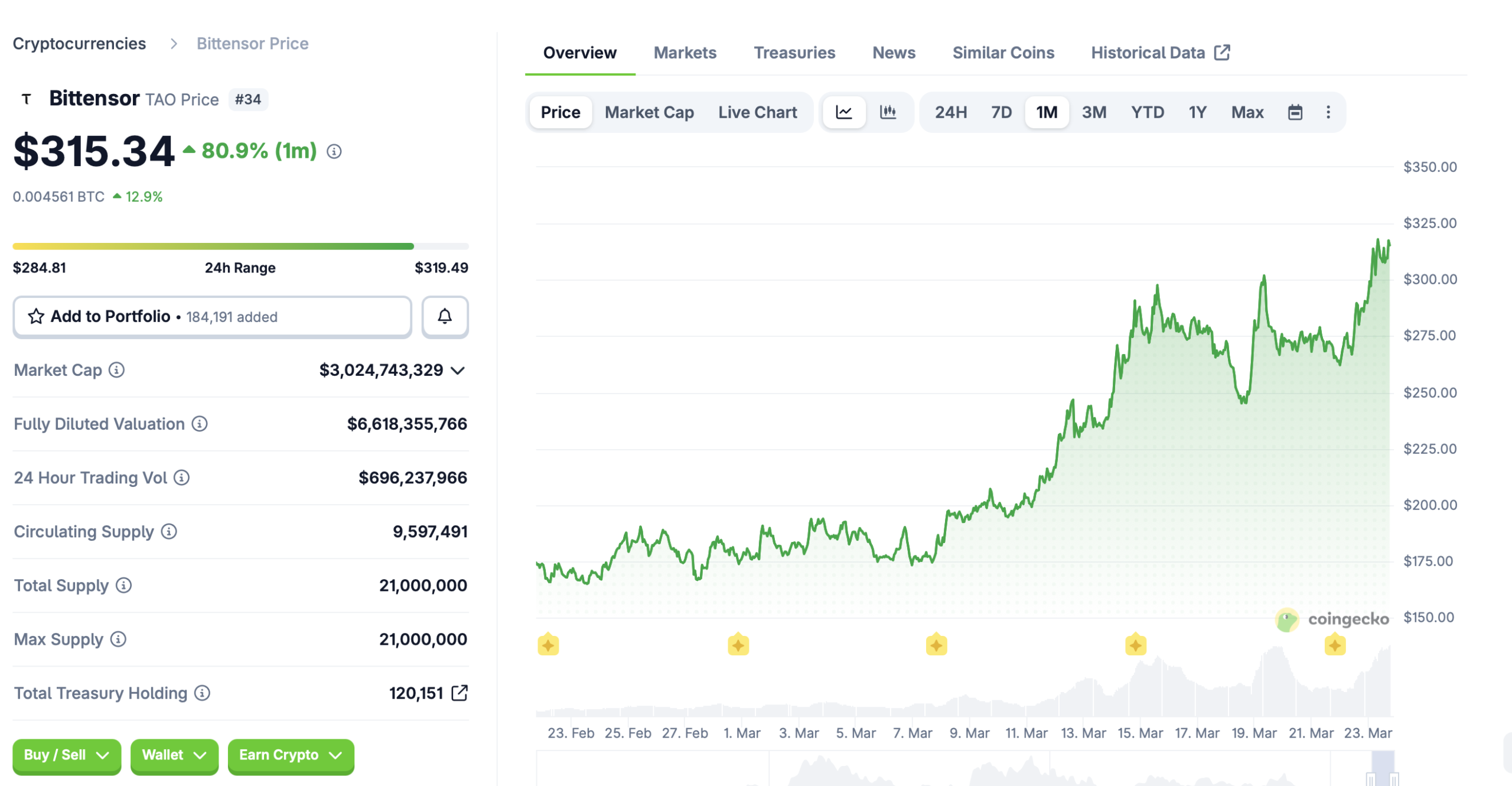

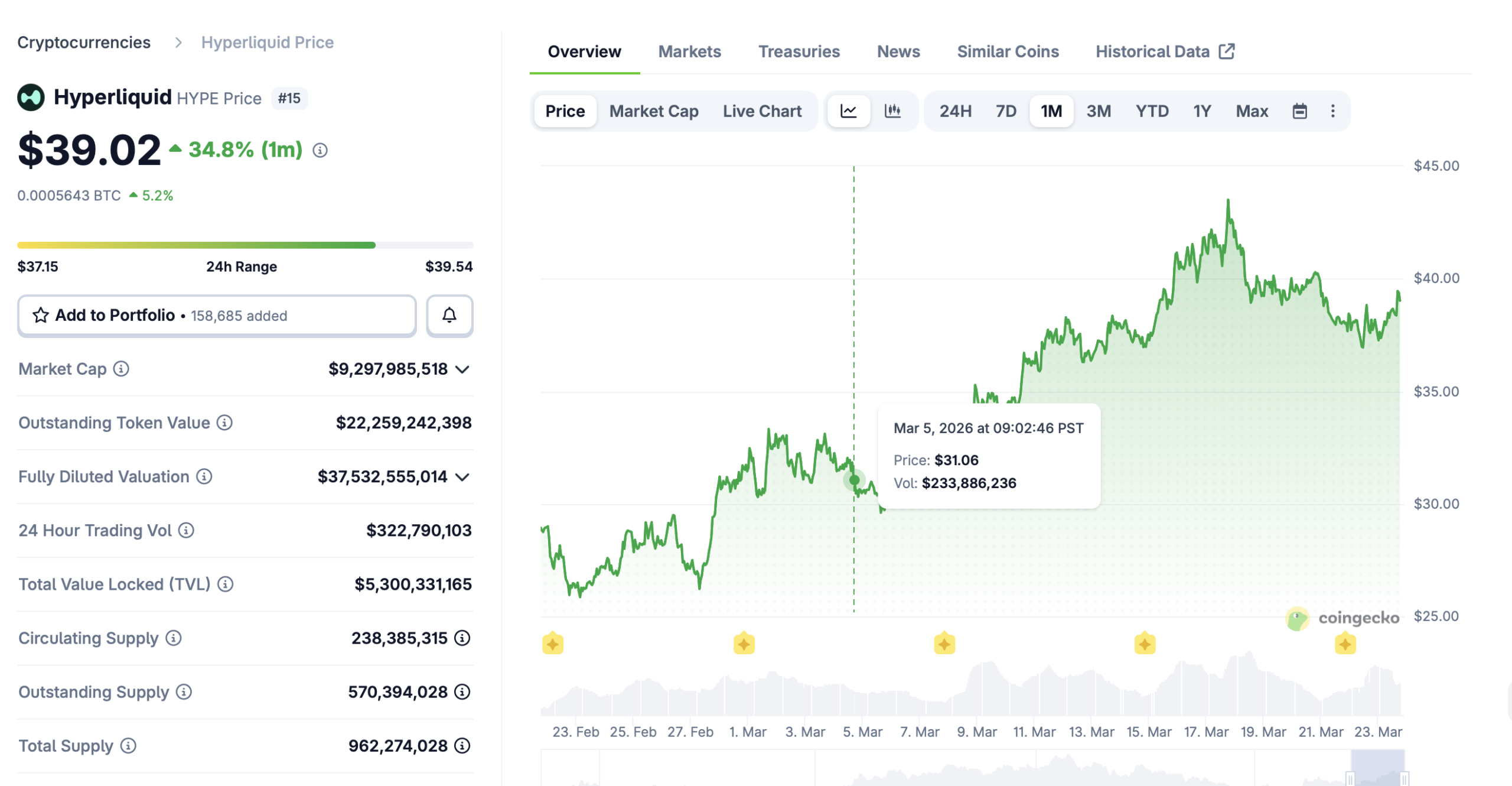

Tokenized gold – the asset you’re supposed to buy when missiles are flying – dropped 14% during an actual military conflict between the US and Iran. At the same time, a decentralized AI network called Bittensor gained 80%, and Hyperliquid, a DEX that most of Wall Street hadn’t heard of six months ago, climbed 34%.

Any financial advisor trained before 2020 would look at that chart and assume the data was corrupted. It’s not.

A Safe Haven That Forgot How to Be Safe

Gold doesn’t go down during wars. That’s been the rule since ancient Rome. You buy gold when the world gets scary. Pension funds know this. Central banks know this. Your uncle who watches CNBC all day knows this.

And yet.

Pax Gold dropped 14.8% over the past month. Tether Gold lost 14.2%. The Strait of Hormuz – responsible for roughly a fifth of the world’s oil shipments – sat effectively closed, while Brent crude traded above $100, while American military assets operated in Iranian airspace.

So what broke? Three forces piled on top of each other, and none of them are obvious at first glance.

The Fed kept rates parked at 3.5%-3.75% on March 18. No surprise there. But the quiet revision – bumping the 2026 inflation forecast to 2.7% – killed the rate-cut narrative overnight. Why sit in a shiny rock that pays nothing when Treasuries hand out 3.5%? Money doesn’t respect tradition. It goes where the yield is.

Gold also had a profit-taking problem that nobody wanted to acknowledge. After a 65% rally in 2025 – a monster year by any standard – institutions were sitting on generational gains. Wars, paradoxically, gave them cover to sell. The same volatility that’s supposed to push gold higher also makes portfolio managers nervous enough to book profits and move on.

And then March 23 happened. Asian equity markets imploded in sequence: Nikkei down 4%, KOSPI down 4.5%, Hong Kong’s HSI down 3.4%. When margin calls sweep through every asset class at once, even safe havens get liquidated. Not because anyone wants to sell gold. Because they have to sell gold to cover losses elsewhere.

The total market cap of tokenized commodities fell nearly 6% in thirty days. This isn’t a PAXG-specific glitch. Gold as a category lost its bid during the exact scenario it was designed to thrive in. It’s like watching an umbrella company go bankrupt during a rainstorm.

Bittensor’s 80% Rally Has Receipts

Our first instinct was to dismiss this as another AI-themed pump. An 80% gain in a fear-driven market sounds like peak speculation. But the on-chain data tells a different story when you actually pull up the receipts.

On March 21 – while most of crypto Twitter was doom-scrolling about Iran – Bittensor’s network quietly finished something remarkable. Over 70 contributors across the globe used standard internet hardware to collaboratively train Covenant-72B, a 72-billion-parameter language model built on 1.1 trillion tokens. No cloud provider. No Google data center. Just regular people with regular computers.

The model scored 67.1 on the MMLU benchmark. For non-ML readers, that puts it roughly in the same league as Meta’s Llama 2 70B – competitive with early GPT-4-class models. A year ago, no serious AI researcher would have believed a permissionless network could pull this off.

Two days before that, Jensen Huang – the Nvidia CEO whose company essentially prints the GPUs powering the entire AI revolution – went on the All-In Podcast and called decentralized AI training “the future of distributed computing.” TAO jumped 17% within hours. Then on March 14, Grayscale filed an S-1 for a spot TAO ETF, which is Wall Street’s way of saying: we need to give our clients access to this.

Social engagement spiked 112% over the month, hitting 3.86 million interactions in a single day. But unlike the typical memecoin pump where engagement runs on bots and paid promotions, this attention tracked actual technical milestones. Product first. Price second.

The Buffett Filter That Separates Winners from Wreckage

Take every token in the top 50 and ask one question: does this thing actually make money? Not “could it theoretically generate revenue per the whitepaper.” Does it produce real fees, today, that you could point to on a balance sheet?

Hyperliquid passes that test decisively. The protocol collected $54 million in fees between mid-February and mid-March – and 97% of that flows directly into HYPE buybacks through their Assistance Fund. Think of it as an automated stock buyback program running on-chain, every day, with no board vote required.

Active traders hit 222,000 – a record. And during the Iran crisis weekend, when CME was dark and traditional commodity exchanges were shut, traders flooded Hyperliquid’s WTI oil perpetuals with $5 billion in volume over 72 hours. You can’t manufacture that kind of product-market fit. Either traders need your platform at 2 AM on a Saturday during a war, or they don’t.

LEO – Bitfinex’s utility token – gained 16.1% on the month through systematic fee burns that shrink supply. It outperformed during every major sell-off this quarter. Not exciting. Extremely effective.

TRON keeps doing what TRON does: processing 7 million transactions daily, hosting $60 billion in stablecoin circulation. Nobody’s making viral posts about TRX. But half the developing world uses it to move USDT, and that kind of plumbing doesn’t break when the Fear index hits 11.

Now flip to the losers. Bitcoin Cash is down 17.5% – still unable to articulate why it needs to exist seven years after forking from Bitcoin. World Liberty Financial, the Trump-branded token, dropped 13.1%. Political branding without utility is just merchandise with extra steps. These tokens failed the stress test because when the tide went out, there was nothing underneath.

Where This Rotation Goes From Here

What we’re watching isn’t a temporary rebalancing. The old model – buy gold when scared, dump crypto when scared – assumed crypto was purely speculative. In 2022, that assumption held. When Terra collapsed, everything went to zero because nothing underneath was generating real economic activity. Just vibes and tokenomics diagrams.

But some of these protocols built actual businesses between then and now. Aave didn’t just survive this drawdown – it attracted capital during it. Hyperliquid didn’t just hold users – it set records. Bittensor didn’t just promise decentralized AI – it trained a competitive model and shipped the proof.

Capital isn’t leaving crypto. It’s leaving the tokens that can’t answer “what do you actually do?” And it’s flowing toward the ones that can point to revenue, users, and shipped products.

Gold, meanwhile, is learning a lesson that crypto learned in 2022: past performance doesn’t guarantee relevance. When a safer alternative with actual yield exists, centuries of tradition can’t hold the bid forever.

Whether this rotation accelerates depends on what happens Friday, when Trump’s five-day Iran pause expires. But the structural shift – capital punishing narratives and rewarding fundamentals – that’s a one-way door. And we’re already through it.

This is not financial advice. DYOR. Data as of March 24, 2026.

Sources

- CoinGecko – Price and market cap data for all assets referenced

- CryptoQuant – Exchange whale ratio, SOPR, exchange reserve data

- CoinDesk – Hyperliquid oil trading volume, JPMorgan analysis

- CNBC – Federal Reserve rate decision, gold market analysis

- CryptoTimes – Bittensor Covenant-72B and Nvidia CEO endorsement

- CoinGlass – Exchange balance and derivatives data